$$ C(S_t,t) = N(d_+) S_t - N(d_{-})Ke^{-r(T-t)} $$ Where N is the c.d.f of the normal distribution.

B.S. formula services as an accurate mathmatical model to price the option, and enbale the people to hedge the risk against almost any underlying assets.

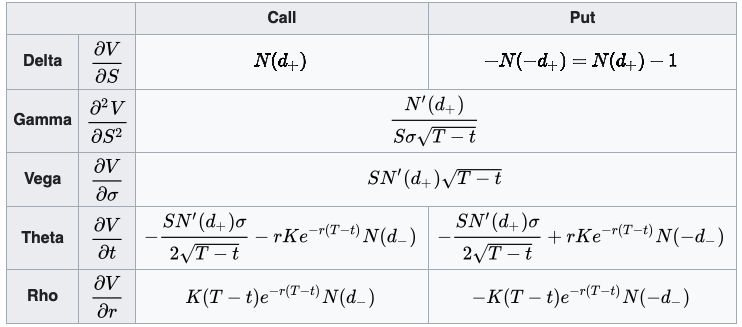

The Greeks for Black–Scholes are given in closed form below. They can be obtained by differentiation of the Black–Scholes formula.

Great Introduction:

https://www.youtube.com/watch?v=A5w-dEgIU1M

To be continued…